(•‿-) Margin Explosion and Transformation to Mid-Tier Producer - Serabi Gold

Sentiment: bullish

This analysis is based on the most recent available data up to June 2026, and all fundamental and operational financial measures in this report are presented in U.S. dollars (USD), as this is the Company’s primary reporting currency. Share prices, market capitalizations and dividend figures refer to the main listing on the London Stock Exchange (AIM) and are quoted in British pence (GBX) or pounds sterling (GBP). The Company’s shares also trade on the Toronto Stock Exchange (TSX) under the ticker SBI and on the U.S. OTCQX market under SRBIF. All derived financial measures, margins and strategic implications reflect the market environment at the end of the first half of 2026.

Company Introduction: Geological Heritage and Strategic Architecture

Serabi Gold plc is a Brazil-focused gold exploration, development and production company. With a workforce of around 1,080 employees, the company operates deep in the heart of the Amazon. Serabi Gold’s entire operations are focused exclusively on the Tapajós mineral belt in the state of Pará in northern Brazil. This decision to concentrate geographically is not a coincidence, but the result of in-depth geological analysis. The Tapajós region is known globally as one of the historically richest, but least systematically explored gold provinces.

The portfolio: Two pillars of growth

The Company’s revenue streams are based on two primary assets that are synergistically linked: the established Palito Complex and the ramp-up Coringa Gold Project.

The Palito Complex forms the financial and operational backbone of the company. For many years, this mine has delivered an absolutely stable, reliable baseload production of about 30,000 to 40,000 ounces of gold per year. This base production acts as a safety net that ensures the company generates adequate cash flows even during weaker periods, but it is not enough on its own to propel Serabi into the league of mid-tier producers.

The real growth engine driving Serabi Gold’s transformation is the Coringa Gold Project. This project, located approximately 200 kilometres south of Palito, was acquired by Anfield Gold Inc. (now part of Equinox Gold) in December 2017 for US$22 million. Coringa hosts high-grade orebodies such as the Serra, Meio and Galena zones. The Company’s strategic goal is to increase consolidated annual production to over 60,000 ounces by 2027 through the expansion of Coringa and to achieve producer status of 100,000 to 200,000 ounces through continued exploration over the next three to five years.

Revenue trends and profit growth (fiscal year 2025)

The full year 2025 marked a turning point. The company produced 44,169 ounces of gold, an increase of 18 percent from the 37,520 ounces in 2024. This increase in volume, coupled with a 45 percent increase in average realized gold price of $3,481 per ounce (2024: $2,407), led to a massive jump in sales. Annual revenue skyrocketed by 65 percent to USD 155.8 million (2024: USD 94.5 million).

The development of profitability is even more impressive: Earnings before interest, taxes, depreciation and amortization (EBITDA) rose disproportionately by 117 percent to USD 77.9 million. Net income reached $53.9 million, an increase of 94 percent compared to the previous year ($27.8 million). Diluted earnings per share nearly doubled to 71.18 US cents.

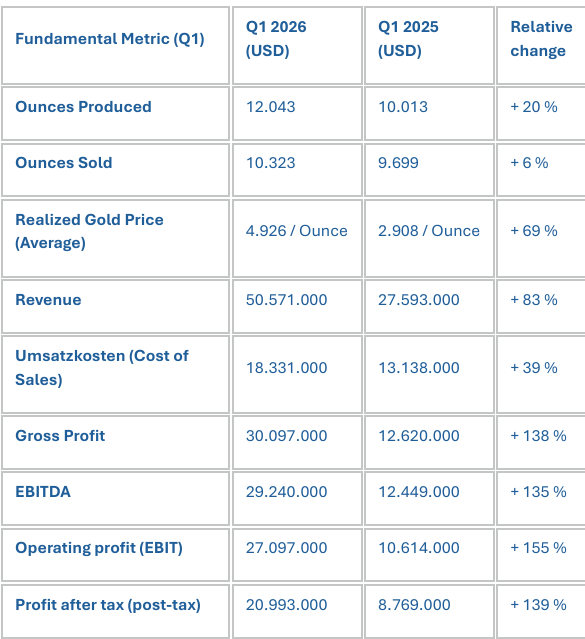

The acceleration in the first quarter of 2026

Financial momentum accelerated further in the first quarter of 2026 (Q1 2026) as the price of gold tested new record levels. The following table illustrates the leverage effect of the sharp increase in margins with only moderate growth in sales volumes.

Although only 6 percent more gold was physically sold in the first quarter of 2026 than in the same quarter last year, sales exploded by 83 percent. This is due to the exceptional average selling price of US$4,926 per ounce that has been realised. These figures objectively prove that Serabi Gold is able to pass rising commodity prices directly into net profit.

The company’s cash generation is simply phenomenal. For the full year 2025, operating cash flow was $55.9 million (up 81 percent from 2024). After deducting mine development costs of $5.3 million, net operating cash flow was $50.6 million.

This massive glut of liquidity has allowed management to completely clean up the balance sheet. In January 2026, Serabi Gold repaid a remaining, unsecured working capital loan of USD 5.3 million at Banco Santander (Itaú Bank) in Brazil. Since that moment, the company has been 100 percent debt-free.

As of March 31, 2026, the company reported a gigantic cash balance of $64.4 million (compared to $49.2 million at year-end 2025 and $22.2 million at the end of 2024). Net cash flow from operations was an impressive $24.2 million in the first quarter of 2026 alone, even after deducting $3.1 million for mine development and upfront costs. Management expects Serabi Gold to generate $80 million to $100 million in free cash flow for the full year 2026 with a continued strong gold environment.

Fundamental valuation: A blatant undervaluation

Based on fundamental key figures, the stock appears grotesquely undervalued on the London and Toronto stock exchanges. At a share price of around 337 to 360 GBX (pence) at the beginning of June 2026, the market capitalisation is only around 272.5 million GBP (approx. 353 million USD).

Subtracting net cash of $64.4 million from this market capitalization, the enterprise value (EV) is just under $290 million. If you put the projected free cash flow of $80 million to $100 million for 2026 in relation to market capitalization, the stock trades with an absurd free cash flow yield (FCF yield) of 22 to 28 percent. According to data providers, the price-earnings ratio (P/E / P/E ratio) is a dirt cheap 5.6x to 6.37x. A company that is debt-free, grows organically and generates almost a third of its stock market value in cash within a year represents classic, deep value play.

Upheaval in the shareholder structure: The Starboard catalyst

In the recent past, a tectonic change in the ownership structure has taken place, which has massive strategic implications. Historically, Greenstone Resources II LP and Fratelli Investments Limited have been the dominant anchor shareholders. In a large-scale transaction, Greenstone and Fratelli together sold almost 21 percent of their shares (15,689,395 shares) to selected British and European institutional investors, as well as around 20 percent to the Classe Roca Magma FIP fund in a separate, binding agreement.

Behind the Classe Roca Magma fund is Starboard Asset Ltda, one of the leading private equity firms in Brazil. Starboard now controls 24.99 percent of the shares in Serabi Gold, while Fratelli continues to hold 10 percent. Other notable institutional shareholders include Ruffer PLC (approximately 4.3%), Gold 2000 (2.4%) and River and Mercantile (1.2%), with approximately 67% of the shares in free float with retail investors and other institutions.

Management rebuild and skin in the game

At first glance, the direct shareholding of the board of directors with only 0.2 percent appears to be a disappointment. However, the Board of Directors has taken drastic measures to enforce the congruence of interests. From 2026, a rigid, binding share ownership policy will apply: Chief Executive Officer Mike Hodgson will be required to build up 150 percent of his annual base salary worth of Serabi shares within five years. The new Chief Financial Officer, Colm Howlin, will have to reach a position of 135 percent of his salary. Until these quotas are met, the company is forcing executives to keep 50 percent of the net shares from all future stock-based compensation. In addition, significant “Conditional Share Awards” were issued on May 12, 2026, the exercise price of which is linked to the volume-weighted average price (VWAP). In addition, financial screeners point out that significant insider purchases were made in the summer of 2026.

Risk analysis: Where are the potential pitfalls?

As flawless as the financial façade may seem, mining in the Amazon region is not forgiving. A merciless analysis reveals three existential risk clusters that have the potential to hit shareholder returns sensitively.

1. Operational and ESG risk: The tragedies of January 2026

The most serious operational risk materialized tragically at the end of January 2026. Within a few days, two unrelated, fatal accidents occurred. On January 25, an employee at the Coringa mine was killed in an accident on the production front. Just a few days later, on January 30, another employee was killed in a traffic-related underground accident in the Palito complex.

The impact of these incidents goes far beyond human tragedy. The affected mining sectors were immediately closed by the Brazilian authorities, including the police, in order to carry out official investigations. Serabi Gold was forced to commission an external audit of its own health and safety processes. In a panic, 7 additional health and safety workers, 4 mine supervisors and a new mine manager were recruited.

2. The Regulatory Sword of Damocles: Coringa’s Approval Cliff

The entire growth scenario of over 60,000 ounces is based on the ramp-up of the Coringa mine. The problem: Coringa does not yet have a final installation and operating license. Currently, the mine is only operating under a three-year trial permit, which expires irrevocably on January 29, 2027.

3. Macroeconomic fragility: What if the price of gold falls?

Currently, the company is highly profitable because the gold price is trading above USD 4,400. However, the cost structure (AISC of $2,293 in the first quarter) gives an idea of how sensitive Serabi is to price declines. If real interest rates in the US continue to rise and geopolitical trouble spots cool down, the gold price could experience a sharp downward correction. If gold falls to even $3,000, Serabi’s margins would shrink drastically. The targeted $80 million to $100 million in free cash flow for 2026 would evaporate, hurting the company’s ability to sustain its ambitious exploration programs and dividends.

Special opportunities and price potential: Why this stock is an “Undiscovered Gem”

Despite the risks involved, Serabi Gold offers a combination of value, growth and catalysts that is rarely seen in today’s mining landscape.

The establishment of a reliable dividend policy

On May 1, 2026, the Board of Directors announced a decision that fundamentally changes the investment case: to pay an annual dividend of 5 pence per share (about 7 US cents) for the past financial year 2025. This corresponds to a total distribution of around USD 5.41 million.

Much more important than this initial distribution is the implementation of the binding capital return policy for 2026: The company has officially committed to returning between 20 and 30 percent of the generated free cash flow to shareholders annually in the form of dividends or share buybacks. If this promise is calculated based on the expected free cash flow of $80 million to $100 million for 2026, $16 million to $30 million would be available for distributions in the coming year. Based on the current market capitalization of around USD 353 million, this would correspond to a dividend or buyback yield of 4.5 to 8.5 percent. This reliable, transparent capital return qualifies Serabi Gold for inclusion in specialized dividend funds, which will put structural buying pressure on the stock.

Upcoming catalysts: What will drive the stock price in the next few months?

A dense news flow is emerging for Serabi Gold for the second half of 2026:

Regulatory breakthrough (H1/Q2 2026): The most potentially price-driving news would be the confirmation that FUNAI has approved the ECI study and that INCRA is clearing the land-use change. As soon as the state environmental agency SEMAS issues the final installation license (LI) for Coringa, the greatest existential risk (the expiration of the GUIA in January 2027) will be eliminated.

Exploration Updates (Q2/Q3 2026): Management has announced a comprehensive exploration update for the second quarter of 2026 that will provide results from the 30,000 metre drill program. Positive drill results from new zones such as Galena fuel the M&A fantasy.

Financial results for the second quarter (end of August 2026): The publication of the Q2 report will have to prove that the enormous free cash flow from Q1 was not a flash in the pan.

Commissioning of the 4th ball mill in Palito (Q4 2026): The planned completion of the mill installation will finally raise the processing capacity to 900 tpd. This milestone marks the moment when Serabi is physically able to run the 60,000 ounce run rate.

Conclusion: The transformation to a highly profitable mid-tier producer

Serabi Gold plc (LSE: SRB) represents an exceptional investment thesis in the middle of 2026. The company embodies the rare case of a gold producer that does not burn the macro euphoria of record gold prices above USD 4,400 in wasteful acquisitions or bureaucratic inefficiencies, but directs it directly into free cash flow via an ingenious, capital-efficient approach.

The fundamental basis is undeniably strong: a flawless cash balance of $64.4 million, zero debt, organic production growth towards 60,000 ounces, a projected P/E ratio in the single-digit range and a contractually anchored dividend policy that distributes 20 to 30 percent of cash flow. The entry of the Brazilian private equity firm Starboard Asset also gives a necessary local political clout.

Current price 5.01 USD

My price target for the next 3 years is 27 USD (+438%).

My basic idea when investing is to buy a stock cheaper than it is actually worth. I work with a “fair P/E ratio” (P/E ratio - price-earnings ratio), which is supposed to reflect the fair value of a stock. If a fair P/E ratio of 15 is calculated for a company and is currently trading on the stock exchange for a P/E ratio of 10, then it would be a cheap buy. The bigger the gap between fair and current P/E ratios, the cheaper I am in purchasing! From this “gap” I calculate the potential for future price gains, because sooner and unfortunately sometimes later, the stock market recognizes the “fair P/E ratio”.

According to my calculations, the “fair P/E ratio” here is 19.2

My investment style is a mixture of value/momentum investor. Based on the fundamental data (VALUE) and the price development of the last 52 weeks (MOMENTUM), the stock is currently one of my TOP 25 stocks. These are the stocks where I see the highest chances of strong price gains in the medium term (1-3 years). I also buy these values in my wikifolios and at FollowMyMoney.

What do you think about the stock? My stock ideas are part of the

“Elite Investor Feed” at ☛ Yellobrick

the performance of my stock ideas is tracked, independently of me. At the moment, it looks like this.

“Speculative investments are like a tennis match: the decisive factor is to concentrate fully on the next ace instead of being annoyed by the last double fault.” A. Gerstenberger

Disclaimer

This text was partly created with AI applications.

All content is for informational purposes only and does not constitute investment advice or a solicitation to buy or sell securities or other financial market instruments. Of course, I try to present the facts to the best of my knowledge and belief, but they can still be false in whole or in part.

Therefore, I do not accept any liability for investment decisions that you make on the basis of the information presented here.

Conflict of interest: At the time of publication, the author of this publication holds shares/securities of the securities/companies discussed here and intends to sell them depending on the market situation and could benefit in particular from increased trading liquidity. As a result, there is a concrete and clear conflict of interest.