Favorable valuation with rapid growth, but there is 1 problem

BQE Water, $BTQNF, $BQE:CA, ISIN #CA0556402059

https://www.bqewater.com/investors-media/

The company

BQE Water is a Canadian-based service provider specializing in water treatment and management for the metal mining, smelting and refining industries. The company provides operational services for water treatment plants and offers technical services in the field of water management. In 2022, the company was recognized as one of the "50 Fastest Growing Green Companies in Canada".

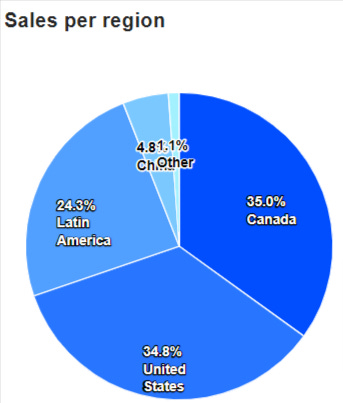

All following currency figures are in CAN $! Most sales come from North America, see chart Sales 2022.

The customers are large commodity companies such as: Glencore, Jiangxi Copper, Freeport-McMoRan, Codelco, Kinross Gold, Centerra Gold, Torex Gold, Teck Resources, Anglo American, Barrick Gold, US Power Utility, Trafigura, Orano, South32...The company is active worldwide with most locations in North America.

Source: Company presentation

The potential

The returns from "typical projects" are as follows.

Source: Company presentation

In the first step before a water treatment plant is installed, one-off consultancy costs of around USD 1.5 million are collected over a period of 5 years. In approx. 15%-20% of cases this becomes a project. If a water treatment plant is operated, recurring income of approx. 1.5 million $ / year is collected over a period of 15 years. If the mine is then closed, the water treatment plant must generally continue to be operated. Further income of approx. USD 2 million is collected over a period of 10 years. The total income thus amounts to approx. 26 million $ over a period of 30 years.

With 4 new projects per year, this results in a sales potential of 2,000 million $ in 20 years. According to the company, this corresponds to a market share of just 0.2%. BQE Water only launched its first projects with recurring revenues in 2020.

The number of active mines worldwide is estimated at around 5,200. The number of mines in development status is approx. 21,000 and the number of closed mines is approx. 52,000, see diagram.

Source: Company presentation

The latest results

The results for Q3 were published on 28.11.2023. The highlights for the quarter:

- Revenue of $8.0 million and $6.2 million in Q3 2023, up 40% and 78%, respectively, from Q3 2022 and both historic highs in a quarter driven primarily by new recurring revenue from operations and growth in technical services in 2023.

- Operating margin of 3.3 million dollars in Q3 2023 compared to 1.7 million dollars in Q3 2022, an increase of 88

- Record high net income of 2.1 million dollars in Q3 2023 compared to 573,000 dollars in Q3 2022, an increase of 272

- Adjusted EBITDA of $2.7 million in Q3 2023 compared to $1.4 million in Q3 2022, an increase of 101%

Highlights for the first 9 months:

- In the first nine months of 2023, we expanded our water treatment services to four different locations in North America and increased our year-to-date water treatment fee revenue to $5.4 million, an increase of $2.6 million, or 94%, compared to the same period in 2022.

- Technical services revenue, which is derived from our specialized professional services in the water industry, has always been a precursor to future operating services. Our technical services revenue increased to $7.7 million year-to-date, an increase of 31% compared to the same period in 2022, due to several major projects we worked on in 2023.

- BQE Water is are pleased with the successful completion of the pilot campaign for a rare earth extraction project in Chile, where the successful integration and implementation of water treatment into the extraction process plays a key role in the granting of the environmental permit for the project.

The fundamental key figures

The fundamental key figures for 2024 (own calculations): P/E ratio (price/earnings ratio) < 8; EV/EBIDTA (enterprise value/EBIDTA) < 5, sales growth 50%.

I expect sales development (in CAN $m) as follows:

Earnings per share developed as follows:

My investment style is a mixture of value/momentum investor. Based on the fundamental data (VALUE) and the share price performance of the last 52 weeks (MOMENTUM), the share is one of my TOP 25 shares. These are the stocks where I see the highest chances of strong price gains in the medium term (1-3 years).

What else is important:

- BQE Water is debt-free and had around USD 6 million in cash as at December 31, 2022. The construction and operating resources for the water treatment plants are paid for by the customer. BQE is paid for its expertise.

- As of mid-2023, the "recurring revenue" was 57%. I expect this percentage to continue to rise. The share of consulting revenues should fall accordingly.

- The share price has approximately tripled since 2020, see chart.

What is the problem?

- Insiders own about 55% of the shares and are not selling any. According to Yahoo Finance, there have been insider share sales in the last 24 months. The free float is therefore very low.

- Even on the home exchange in Toronto, turnover is low. The average volume in Toronto in the last 3 months was 554 shares. With approx. 200 trading days, that would be an annualized volume of approx. 111,000.

- On 6.12.2023, BQE Water announced a further share buyback program. As part of the normal issuer bid, the company will buy back up to 62,351 (approx. 55% of the projected annual volume) shares, which corresponds to 5% of the issued share capital. The repurchases will be funded from the Company's existing working capital. All repurchased shares will be canceled. The plan will be valid until December 13, 2024. As of November 29, 2023, the company had 1,247,028 shares issued and outstanding. The buyback program should support the share price downwards. However, the number of shares tradable on the stock exchange will be further reduced.

- There are therefore hardly any shares to buy. Therefore, if you want to buy here, always order with a limit and be patient!

Conclusion

Water treatment is an important topic for the future that offers far-reaching potential for alleviating water scarcity, using raw materials responsibly and reducing energy consumption. BQE Water operates in a "blue ocean" market. "Blue oceans" are understood as untouched markets or industries that have little to no competition. BQE has its own patents and the market appears to be huge. There seem to be plenty of opportunities for high profitable growth. The major shortcoming of the share is the low free float.

Possible Trigger: Quarterly report estimated 2.April 2024

Thanks for the thesis.

The TAM should be adjusted IMO. Instead of calculating the total amount of mines, better to ask, how many of the total mines are eligible to use their solutions? E.g. is it all type of mines that are potential candidates, including coal, metal, nonmetal, stone and sand&gravel? These should then be excluded. Then one should also consider how large the miners should be in order for their solutions to be cost-effective for the miners, instead of just getting rid of the water in some other way.

The next thing that should be adjusted IMO, is the revenue per captured project. If we assume they capture 4 miners per year, but only 15% of these become projects, then I get the following calculation:

4 proj/yr * 20yr * ($1.5M*5yr+0.15* ($1.5M * 15 yr + $0.2M*10yr)) = $894M. I.e., roughly $1B in recurring revenue for 20 yrs. They captured 3 projects in 2022 and 2 projects 2023. Assuming they capture 2-3 per year instead we get $500-750M instead. Still good, considering they have $16.6M TTM of revenue today so a 30-60 bagger in 20 years (12-15%CAGR), assuming same multiples and magins as today, IF nobody else is able to develop a better solution during these years or if they go private/aquired.